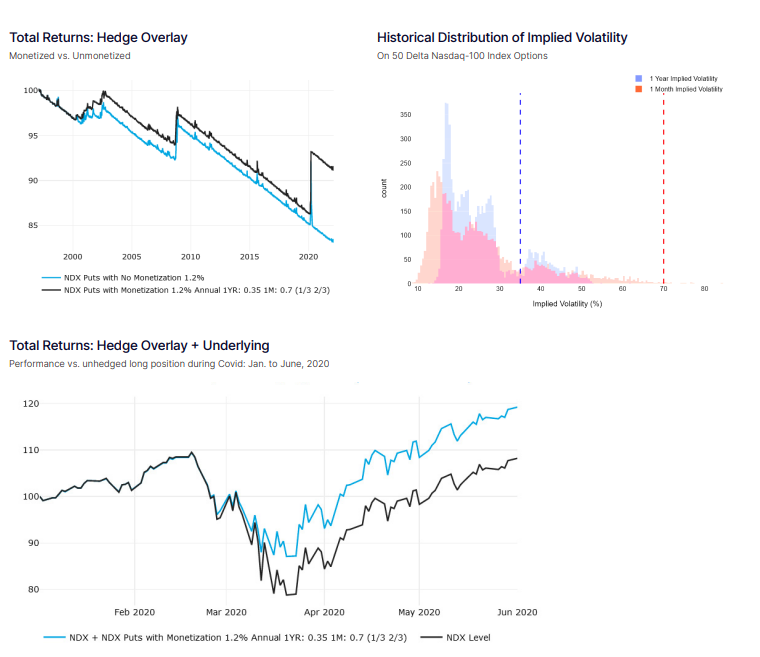

We explore the effects of an implied volatility based monetization scheme on a laddered put strategy on the Nasdaq-100 Index (NDX). The strategy holds 1, 2, and 3 month put options on NDX struck 20% out of the money. We purchase new 3 month puts at each third Friday expiry, spending 10bps per month (1.2% annually) of a total portfolio notional. We also analyze performance with a joint long position in NDX to demonstrate the value of systematic monetization of options contracts to lock in gains from adverse market events. Specifically, when a monetization event occurs, proceeds from the sale of puts are stored in an interest bearing cash account until the next roll day when proceeds are invested firstly into a new 3 month put and the remainder into NDX. Implied volatility is referenced as the 50 delta 1 year implied volatility and the 50 delta 1 month implied volatility. The study period ranges from January 1st, 1997 to February 15th, 2022.

We found that there was a significant benefit to including an implied volatility based monetization scheme in reducing impact from market drawdowns. In our study, monetization served as an effective mechanism to capture gains from adverse market events. We found that the monetized strategy reduced annual volatility by 115bps while returns were reduced by only 2bps. By contrast, the unmonetized strategy was effective in reducing risk, but with significant cost as annual returns were lowered by 52bps.

As a standalone overlay (i.e. not including the underlying asset), the monetized strategy outperformed the unmonetized version on a cumulative basis. The unmonetized strategy realized cumulative returns of 16.78% while the monetized strategy realized cumulative returns of 8.77%. The maximum 1 month return of the monetized strategy was 6.26% vs. only 1.89% in the unmonetized strategy.

Historical and simulated index performance is not necessarily indicative of future results. The information provided in this document does not constitute investment advice. Volos is not an investment advisor. Volos and its affiliates accept no responsibility whatsoever for any loss or damage of any kind arising out of the use of any part of the company products or the information contained therein.

© Copyright 2022. All rights reserved. Nasdaq is a registered trademark of Nasdaq, Inc. 1473-Q22

Harold is the architect of Transtrend’s Diversified Trend Program, responsible for R&D, portfolio management and trading. Harold was born and raised on a dairy farm in Drenthe. And from a young age, he has been intrigued by linking mathematics to the real world around us.

He graduated in 1990 with a Master’s degree in Applied Mathematics from the University of Twente in the Netherlands. In the final phase of his studies, while working on the project that would later become Transtrend, he became fascinated by the concept of leptokurtosis — or ‘fat tails’ — in probability distributions, a topic which has inspired him throughout his career.

Harold’s approach to markets is best described as a combination of a farmer’s common sense and mathematics, never losing sight of the underlying fundamentals.