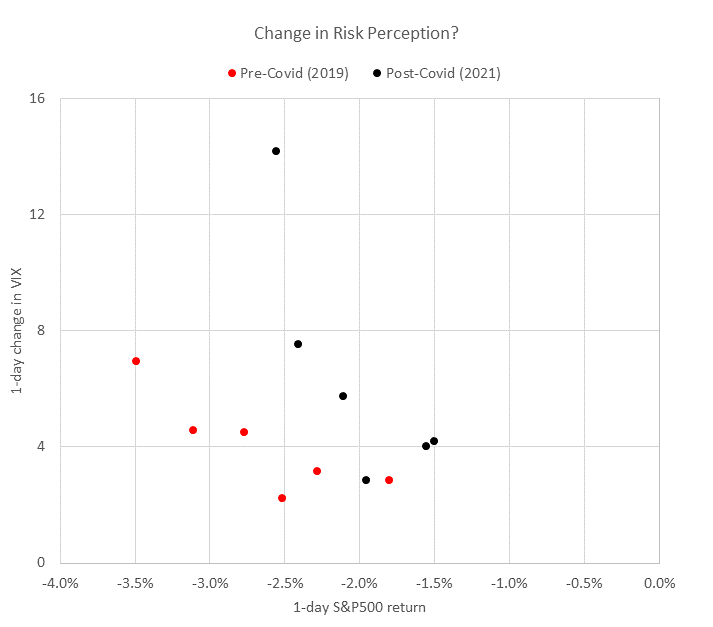

Markets are well on their way to posting another record year and the Covid crash now looks like a blip, albeit a big one, in the unstoppable rally. But is there more to this than meets the eye? We plotted the worst S&P500 daily returns from January to August 2019 versus the daily changes in the VIX and compared this to the data from the same period in 2021. An elevated nervousness in the post-Covid era is clearly observable – the jumps in the VIX are higher on the days when the S&P500 is down. Some of the likely reasons for this change in the risk perception are not only related to the lingering memory of the Covid crash, but also due to the increasing concerns related to the withdrawal of the supply of liquidity and increasingly stretched equity valuations.

Harold is the architect of Transtrend’s Diversified Trend Program, responsible for R&D, portfolio management and trading. Harold was born and raised on a dairy farm in Drenthe. And from a young age, he has been intrigued by linking mathematics to the real world around us.

He graduated in 1990 with a Master’s degree in Applied Mathematics from the University of Twente in the Netherlands. In the final phase of his studies, while working on the project that would later become Transtrend, he became fascinated by the concept of leptokurtosis — or ‘fat tails’ — in probability distributions, a topic which has inspired him throughout his career.

Harold’s approach to markets is best described as a combination of a farmer’s common sense and mathematics, never losing sight of the underlying fundamentals.